After a slight break, I’m back with more Freelance Finance! To recap, in this series I write about very basic finance for beginners. As before, this is not so much financial advice, but an introduction to a bunch of concepts, that you should always adjust to fit your own needs.

Previously I introduced the concept of “buckets”; where you split all incoming payments into groups based on your needs and goals. This post focuses on the Spending bucket, breaking your spending down into smaller categories to help track where your money goes.

Illustration from Tales by the Brothers Grimm, 1917 – Arthur Rackham

Tracking Your Monthly Spending

In my last post, I discussed having a Surplus bucket, from which you pay yourself a “monthly wage”. How much you pay depends on your budget, and that’s where tracking your monthly spend comes in!

I have (yet another) handy spreadsheet for this: Click here for the spreadsheet (remember to save your own editable version by going to File>Make A Copy).

Fill in the spreadsheet by looking through your bank statements from all your spending sources (bank accounts, PayPal, etc.), and categorising each purchase. While I’ve listed some example categories, these will need to be personalised as it is so subjective. Try to group purchases that seem intuitive to you, and add as many categories as you need.

To get a more accurate idea of your spending, consider looking at 3 months of bank statements and coming up with a monthly average for each category. If you’re ambitious, you could also average out a whole year’s worth of spending – this will be helpful as spending can fluctuate depending on the time of year.

Time Is Money, 1894 – Ferdinand Danton Jr.

Ranking Your Spending Categories

Once you have your categories, you can assess the importance of each by ranking them in tiers:

Critical: Essential for survival (food, shelter, medication, etc).

Need: Still important, but manageable if you have to do without.

Want: Non-essential indulgences, or upgrades to things in your Critical & Need tiers (for example, while groceries in general should be Critical tier, fancy coffee might be a Want).

In the spreadsheet, you can use the dropdown on the right for ranking each category. At the bottom of the page, there is a summary which tells you exactly how much you are spending per month on your Critical expenses, Needs, and Wants!

Again this will be highly subjective, but do your best to rank your categories, as there are no wrong answers.

CPA (Daydreaming Bookkeeper), 1924 – Norman Rockwell

Making Adjustments & Budgeting

With the hard work out of the way, you can look through your spending categories, and make some adjustments if needed. Going through your spending line by line like this really forces you to consider what is necessary, and you’ll soon notice areas where you can cut back, and areas that could use more funds.

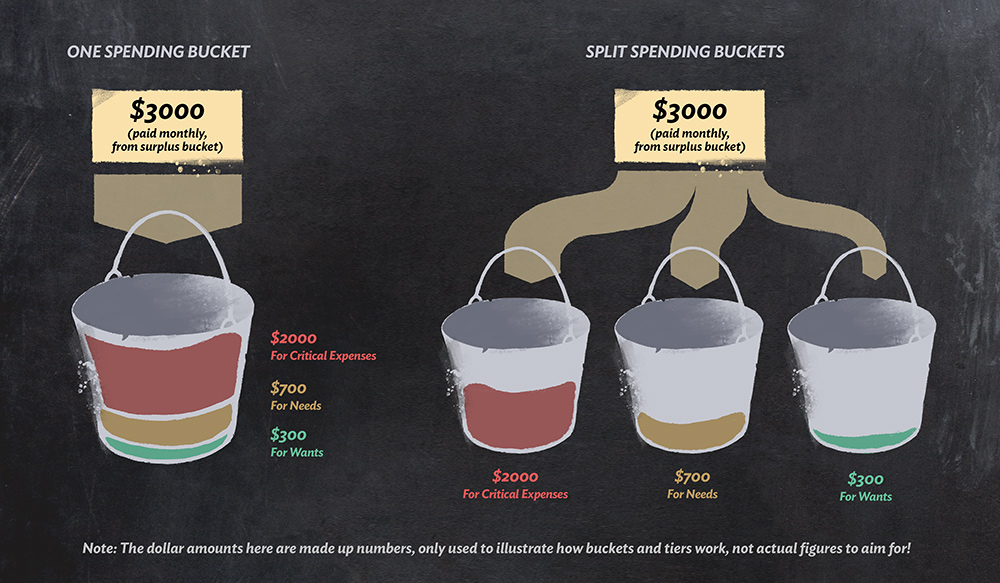

To tie it all back to buckets, this ranking system basically splits up your Spending bucket by importance, and informs how much to pay yourself from your Surplus bucket. For most people it’s enough to just know a rough breakdown, and have all spending money come out of the one bucket, but you could choose to have separate spending buckets based on these rankings, if you prefer a structured approach and don’t mind having too many buckets!

Since illustration income is often irregular and you can’t expect a set amount every month, traditional budgeting with strict numbers may not work well. But what could work is portioning every payment into buckets, and ranking your monthly spending by importance. With these measures in place, you can gain a clear picture of your finances, which can in turn actually help you plan the jobs you accept.

Planning ahead

Using the amounts from your rankings, you can estimate how much money you’d need in a year. For example, if your Critical tier adds up to $2,000* a month, you know you’d need $24,000 a year (after tax, retirement fund, etc) to survive. So you can set that as a financial goal, followed by the amounts that would cover your Needs tier, and then your Wants tier for the year.

With these goals in place, let’s say you take a large job and earn that 24k in the first half of the year – this essentially means that you’re set for the rest of the year! From there, knowing all your critical spending is covered, you can choose to keep taking on jobs and clear your Needs and Wants tiers as well, and start putting away extra money into savings, or you could afford to be more picky about the types of client jobs you accept, and even take some time off to work on some personal projects.

* All numbers used in these examples are completely made up, and not meant to reflect actual living costs!! You need to track your own spending to figure out the real numbers!

Illustration from Howard Pyle’s Book of Pirates, 1911 – Howard Pyle

While the bucket system is something to establish and use consistently, tracking your spending is a more occasional task. You don’t need to scrutinise every cent you spend every single day, but hopefully, this post has highlighted the value of checking in from time to time, to see how you are spending your hard-earned money!

Freelancing can often feel uncertain; like you never know if you’re making enough. However, by categorising and ranking your spending, you can determine exactly what enough means for you, and use that knowledge to inform your financial goals and the types of jobs you pursue.

Woman Holding a Balance, 1663 – Jan Vermeer

This post is part of a Freelance Finance series:

1 – Bookeeping

2 – Buckets

3 – Budgeting (You are here)

{kind=link}

Recent Comments